Blog

Beyond Pink: The Unique Role of DFS in Women’s Lives

Explore how thoughtful, context-aware digital financial tools can transform access for women in the developing world. —This post shows how DFS can support women by honoring informal networks, prioritizing privacy, and enabling financial autonomy

In many parts of the world, particularly in Pakistan, women’s mobility is often limited due to cultural and societal norms. Traditional banking services , which typically require in-person visits, inadvertently create barriers to financial inclusion. When mobility is restricted, access to financial services becomes a privilege rather than a right, excluding women from systems designed to empower. Digital Financial Services (DFS) present a paradigm shift: instead of expecting women to reach financial services, they bring these services directly to women, wherever they are.

By rethinking where and how access happens, DFS opens the door to financial inclusion for women who have long been kept at its margins. As designers, we must recognize this potential and responsibility. Inclusive access isn’t just a question of technology—it’s about designing with empathy, nuance, and context.

Financial Inclusion Isn’t New—It’s Evolving

Long before apps and digital wallets, women created their own systems of financial security. In Pakistan, “committees” (ROSCA—Rotating Savings and Credit Associations) have long been trusted networks for saving, lending, and achieving personal financial goals. These systems are not just functional—they are embedded in social trust, discretion, and community solidarity.

Globally, variations of these models have existed for decades—from “tandas” in Mexico to “chit funds” in India and Self-Help Groups across South Asia. They highlight a vital insight: women have always been financially active, but on their own terms, in systems that respect their rhythms and responsibilities.

However, the leap from analog to digital hasn’t always honored these origins. Many DFS platforms fail to acknowledge the informal yet highly effective financial behaviors women already practice. This results in solutions that feel alien, opaque, or even risky to the very people they’re meant to empower.

True innovation lies in building upon these informal networks rather than replacing them. It means digitizing with dignity—retaining the privacy, flexibility, and mutual trust that define women-led financial ecosystems, while layering on the power of scale, accessibility, and autonomy that digital platforms can offer.

From Exclusion to Empowerment: The Design Imperative

Women’s exclusion from formal financial systems isn’t merely a result of policy gaps—it’s a reflection of design oversight. When DFS platforms assume access to smartphones, uninterrupted internet, individual IDs, or formal income documentation, they exclude a vast population of women who may not meet these criteria but still actively manage money, save, invest, and support families.

This isn’t just a user experience flaw—it’s a systemic failure with real consequences. Women may feel, “This isn’t for someone like me.” And when products fail to reflect their realities, trust erodes. The result? Low adoption rates, minimal engagement, and missed opportunities for both women and service providers.

At Ideate, our research revealed that many women still choose to visit banks in person, even when DFS options are available. This isn’t resistance to technology—it’s a need for trust, a sense of credibility, and emotional reassurance. Without these, digital convenience becomes irrelevant.

Designers and innovators must shift from a tech-first mindset to a human-first one. This means deeply understanding the lived experiences of marginalized communities and women—across geographies, class, and age—and designing tools that fit into their lives, not ones that expect them to change to fit the tools. At Ideate, we’ve spent over seven years collaborating with banks, fintechs, and microfinance institutions across Pakistan. Our fieldwork has shown that creating truly inclusive digital financial tools requires thoughtful, context-aware design—not just branding with feminine colors or names.

Here’s what we’ve learned.

Key Principles for Designing Women-Centric DFS Platforms

Intuitive and Simplified Navigation

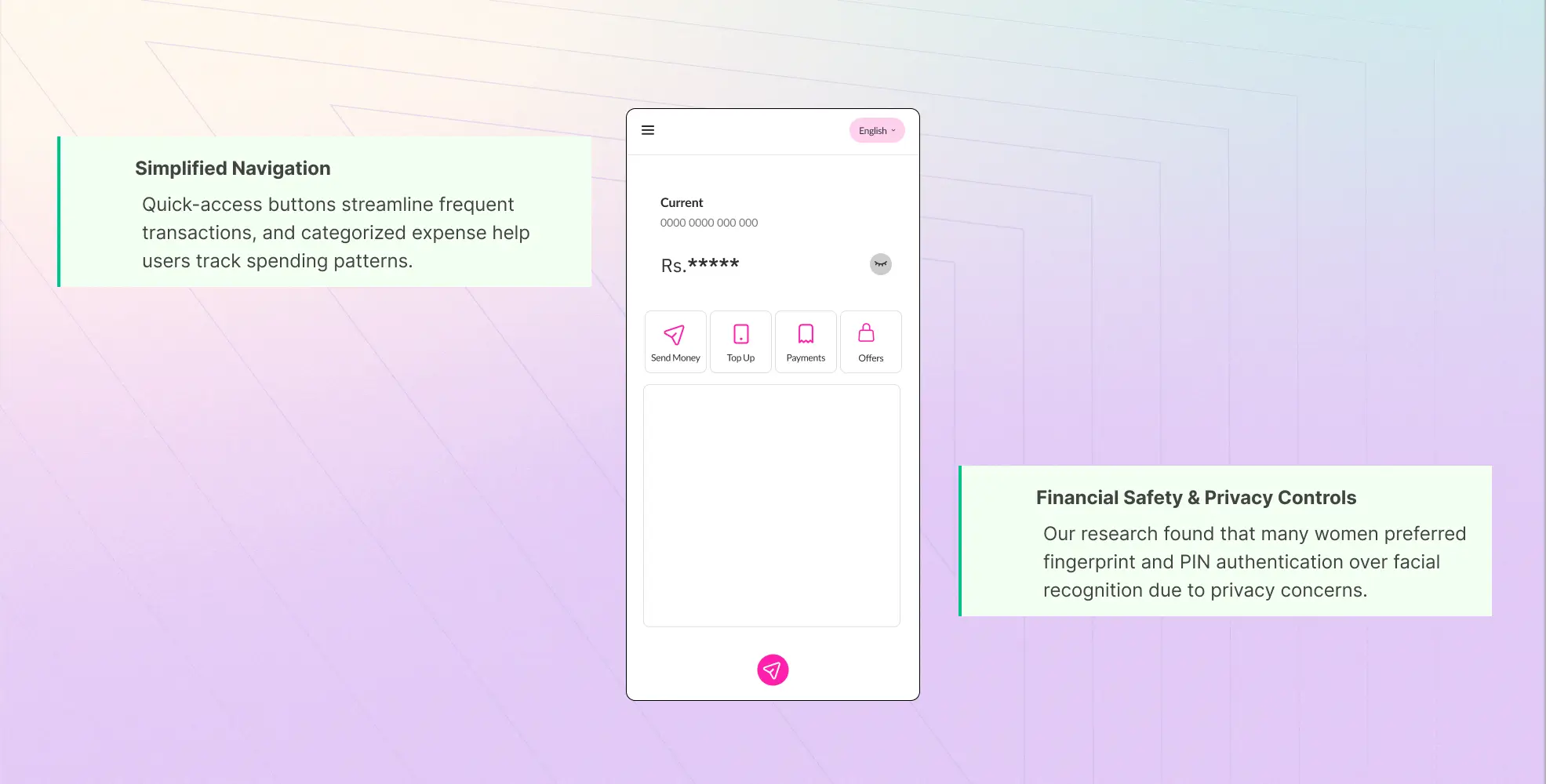

Women often juggle multiple responsibilities and need quick, seamless access to financial tools. A minimalist dashboard that displays essential features such as account balance, recent transactions, and bill payments is crucial. Quick-access buttons for frequent transactions simplify financial management, while categorization of expenses into sections like healthcare, education, and savings helps users understand their spending patterns.

Financial Safety & Privacy Controls

Security concerns are one of the biggest barriers preventing women from engaging with digital financial services (DFS). Features like biometric authentication - such as fingerprint and facial recognition - offer enhanced security, while a discreet mode allows users to hide sensitive financial details when using the app in public. Our research found that many women preferred fingerprint and PIN authentication over facial recognition due to concerns about privacy breaches associated with facial recognition technology. Providing a variety of security options is essential to building trust and ensuring that women feel safe using digital financial services. This was a key learning from our project with community banks, where we incorporated feedback to enhance privacy and trust features.

Personalized Financial Insights & Education

Many women seek financial literacy but often lack tailored educational resources. Goal-based savings tools enable users to set and achieve financial milestones, such as saving for education, business investment, or maternity expenses. A dedicated financial education section provides bite-sized content on topics such as credit scores, investing, and wealth-building. Spending insights offer personalized spending reports and budgeting tips, helping women make informed financial decisions.This insight came from a project where we tested educational content for female users in rural areas, emphasizing bite-sized, accessible information. Through projects like Evaluating the Impact of a Financial Inclusion Program on Female Micro Entrepreneurs (BopInc & JazzCash), we gained critical insights into the importance of designing a last-mile distribution model that provides low-income women with employment opportunities and expands their financial inclusion. Our qualitative research focused on understanding the impact of the JazzCash partnership on female micro-entrepreneurs across various provinces, allowing us to better understand the barriers and needs that these women face in accessing digital financial services.

Building Trust through Community Engagement and Peer Support

Women are often hesitant to adopt digital financial services due to past negative experiences or limited exposure. Many prefer community-led financial practices such as informal savings and cash transactions over digital platforms. Financial institutions can build trust by leveraging peer recommendations, launching community-based marketing campaigns, and partnering with credible local organizations to promote DFS adoption.

During our project, Helping Low-tech Women Become Digitally-enabled Entrepreneurs (Unilever’s Guddi Baaji Program, IDEO.org & Finja), our journey mapping, persona creation, and prototype testing aimed to empower rural women through digital entrepreneurship. Through this work, we learned that enabling women to access stock-on-credit solutions and become mobile money agents requires more than just introducing technology. It demands comprehensive support and community engagement, addressing the real-world challenges women face in accessing digital services.

Time-Saving Features for Busy Women

With demanding schedules, women need banking solutions that prioritize efficiency. Scheduled payments and automated reminders help users avoid missed transactions along with incentivized payments encourage women to use their app for repeated transactions. Additionally, split-bill functionality makes it easier to manage shared expenses among family and friends, reducing financial stress.

Financial Incentives to Boost DFS Adoption Among Women

Women are more likely to adopt DFS when clear financial benefits are offered. Incentives such as reduced transaction fees, cashback rewards, or targeted training programs increase adoption rates. Financial institutions should design simple, transparent incentive structures that directly link to tangible financial benefits, making DFS more appealing to women users.

In our project Creating Communication & Incentive Strategies to Increase Women Micro-entrepreneurs’ Digital Financial Inclusion (Mobilink Microfinance Bank, 2024), human-centered innovation sprints were conducted to co-create incentives and communication strategies to increase awareness and engagement with digital financial tools among women micro-entrepreneurs. This project has reinforced the need for clear, accessible information and tailored incentives to engage women users.

Community & Support Features

A strong sense of community fosters trust and engagement in digital financial services. Women-focused investment forums provide a space for discussions on wealth-building strategies. Dedicated customer support ensures users have quick access to financial advisors, while mentorship programs connect women entrepreneurs with experts to guide their business and financial decisions. By integrating these features, banks can build stronger relationships with women users and encourage long-term engagement with digital financial tools.

Understanding Gendered Products and Designing for Actual Needs

Many digital financial services claim to be “women-centric” but rely on surface-level branding—most often, pink palettes and floral motifs. This aesthetic shorthand, rooted in mid-20th century marketing norms, assumes that femininity equates to a specific visual identity. While intended to appeal to women, it often ends up reinforcing outdated gender stereotypes.

Our research—and that of others—shows this approach doesn’t resonate with all women. In fact, it can obscure the deeper, functional needs that matter more: privacy, security, intuitive interfaces, and meaningful financial education. When design prioritizes visual cues over usability, it signals that the service is more about image than real value.

A study in Cultural Trends noted that while pink may visually suggest femininity, it rarely translates to genuine engagement, especially when it overshadows practical features. This reinforces a key insight: branding alone doesn’t build trust—usefulness does.

By designing digital tools that truly reflect women’s economic roles, personal contexts, and financial goals, we move beyond superficial inclusion toward real empowerment. The goal isn’t to wrap old systems in new colors—it’s to reimagine financial services that speak to the complexity, capability, and agency of all women.

It's essential to recognize that a banking app is not a product to be marketed; it’s a service designed to meet real financial needs. Simply changing the color palette or using catchy names is not enough. To truly serve women, DFS platforms must consider security, ease of use, trust-building features, and relevant financial education. The service should be designed to cater to their specific life circumstances, making financial tools genuinely accessible and meaningful. Only then can we move beyond the "pink" approach to creating financial ecosystems where women feel empowered, secure, and in control of their finances.